Growth belts: mapping an overland future for Asian tradeThe EIU

When a block train set off from Amsterdam on March 7, 2018, bound for Yiwu, China, it established yet another rail link between China and Europe. Since 2011, over 6,000 such trains have been quietly criss-crossing the Eurasian continent, carrying a range of products—from electronics and sporting goods to fresh food and car parts, among others.

The rise of this overland Eurasian freight corridor signals an important shift in the direction of trade. It used to be that, compared with their ocean-facing peers, landlocked countries in Asia struggled to create the kind of rapid industrialization that boosts living standards. Thanks to a host of infrastructure upgrades and technological improvements, however, that is changing: trains can now make an 11,000-km journey in a mere 16 days, almost twice as fast as by sea and more than 70 percent cheaper than by air. The Belt and Road Initiative (BRI) through Central Asia has also contributed to this evolution.

This article examines the old Silk Road countries in Central Asia to argue that their relative isolation is no longer an impediment to greater integration into global trade networks, thanks to improvements in rail infrastructure. The future of trade in Asia may thus be as much a dry-land story as a water-logged one.

Trade torpidity

Among the most isolated areas in the world, Central Asia has only recently started to connect with wider Eurasian trade corridors. Its geographic distance to export markets has always been a drawback but the “economic distance,” as measured by costs and ease of doing business, has been exacerbated by a number of transport-related issues since countries in the region gained independence in 1991.

Infrastructure and equipment, although extensive, have been poorly maintained due to persistent under-investment. Customs procedures and standards in many Central Asian nations are not harmonized, while clearance times, which take less than an hour on average in EU nations, can take days. The need for unofficial payments or extra security increases costs. The result is that transport prices in the region are on average three times higher than in developed countries.

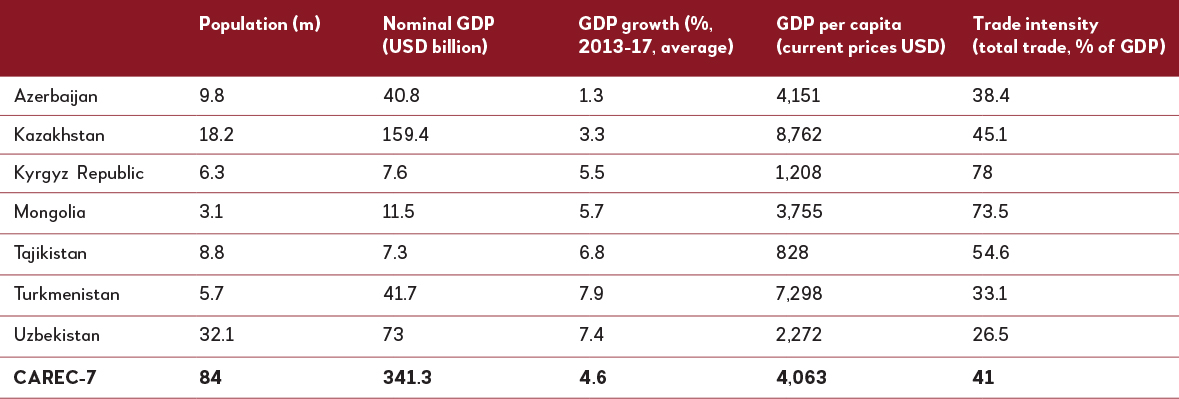

And yet, given its natural resource endowments, relatively numerate and literate populations and proximity to huge markets, the region should be prospering. Many of the region’s exports are generally high-value, hard-currency-earning commodities that could be easily transported by pipeline and rail: oil, iron, steel and copper in Kazakhstan; gold, cotton and oil in Uzbekistan and gas, oil and cotton in Turkmenistan. Following in the footsteps of Southeast Asian countries in particular, they should be able to use the capital gained from the sale of these exports to develop scale-driven resource-processing and assembly-based manufacturing. However, they will need better transport and logistics infrastructure, both hard and soft, to improve trade openness and support industrial upgrading, as suggested by trade intensity data in Table 1.

Table 1: Stuck in a rut? Select economic indicators, CAREC-7,* 2017

Source: EIU calculations using data from “Asian Economic Integration Report 2018,” ADB.

* CAREC-7 excludes some economies which are part of the broader Central Asia Regional Economic Cooperation bloc.

Power in numbers

Partially to address these issues, the Central Asia Regional Economic Cooperation (CAREC) program was started in 1997 to promote linkages between Kazakhstan, Kyrgyz Republic, Uzbekistan and the Xinjiang region of China. In a sense, it follows the same logic that has driven growth across East and Southeast Asia: if you build it, they will come. Infrastructure investment and economic development go hand-in-hand, and the export-oriented manufacturing that worked well for the “East Asian miracle” countries should benefit others in Asia, too.

The goals and structure of CAREC reflect those of other regional cooperation initiatives in Asia, such as the Greater Mekong Subregion (GMS) comprising Vietnam, Cambodia, Lao PDR, Myanmar and Thailand, as well as the southern Chinese provinces of Yunnan and Guangxi, and the South Asia Subregional Economic Cooperation (SASEC) program consisting of Bangladesh, Bhutan, Myanmar, the Maldives, Nepal, India and Sri Lanka. They all aim to create transnational economic corridors through the provision of physical infrastructure, particularly in transport, and connect cross-border markets, production processes and value chains through the movement of people and goods.

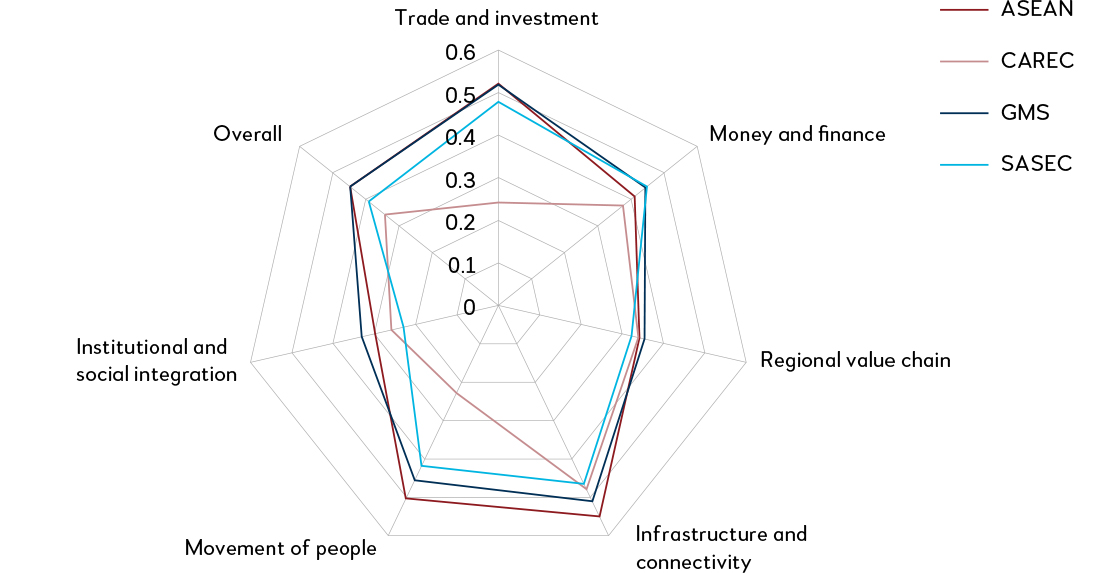

And all three are project-based initiatives, driven by multilateral development banks, designed to improve cross-border connectivity through the provision of infrastructure, boost trade among member countries and strengthen regional economic corridors. However, of the three, GMS has been the most successful in bringing economic development and increased trade to its members. CAREC remains less integrated in terms of trade and investment, as compared to other regions (see Figure 1).

Figure 1: Asia-Pacific Regional Cooperation and Integration Index, overall and by subregional initiatives, 2016

Source: ADB data, https://aric.adb.org/database/arcii; a higher score represents greater integration.

Shoots of progress

The GMS’s success has been supported by wider ASEAN efforts to foster regional cooperation and integration among member nations. It also has benefited from its member countries’ proximity to trade routes, deep-water ports and a prolonged period of peace, which encourages long-term infrastructure development and an expansion in trade flows between countries.

In SASEC, meanwhile, India—by far the most dominant country in the bloc—has not traditionally had the same success in developing overland trade with its neighbors. India’s trade is mainly with other countries, with about 95 percent of India’s trade flowing via one of its many ports so overland border areas have not been a focus.

Yet there are signs this is changing. Since Narendra Modi became prime minister in 2014, India has rebooted its “Look East” policy—now called Act East—to improve connectivity with ASEAN nations. “India is playing catch-up on this but it’s now coming to the party,” says Mark Moseley, COO of the Global Infrastructure Hub, a G20-sponsored think-tank specializing in infrastructure development. “The new government is focused on infrastructure more than previous governments have been.” It will probably need to be in order to increase SASEC’s overall trade as a share of GDP, which at 30 percent is the lowest of the three regional cooperation initiatives.

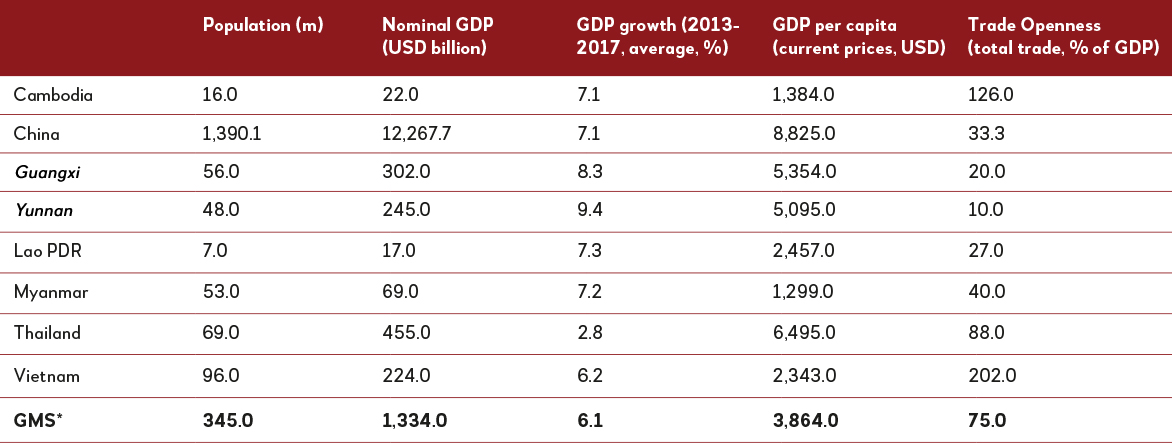

Table 2: Select economic indicators, GMS, 2017

Source: ADB. Asian Economic Integration Report 2018.

* For this computation, GMS includes Cambodia, Yunnan Province and the Guangxi Zhuang Autonomous Region in the PRC, the Lao PDR, Myanmar, Thailand and Vietnam.

A new nerve center?

What could be a game-changer for CAREC? Many point to the launch of the Belt and Road Initiative (BRI) in 2013, which has created opportunities for some countries to slot into emerging East-West trade transit. As a result of widespread investments by China, a number of Eurasian freight corridors are set to expand in the future (see Figure 2). The northern routes—through Russia, Kazakhstan, Belarus, Poland and Germany—have the best infrastructure and are the most reliable and therefore busiest. The southern routes, which will include Uzbekistan, Turkmenistan, Iran and the Caucasus countries, are not yet fully operational due to weak infrastructure and limited capacity.

Figure 2: Eurasian freight corridors and gauges

Source: UIC/Roland Berger. Eurasian rail corridors: What opportunities for freight stakeholders?

The northern corridors have seen investment in railway infrastructure and terminals, an expansion in the number of destinations in China and the EU—about 35 each at the time of writing—and train service, although that still runs largely on an ad-hoc basis. Journey times have shortened by two days since 2011. As a result, cargo movements have increased—from 25,000 TEU in 2014 to 240,000 TEU in 2017. They are expected to grow further, to 636,000 TEU in the next 10 years.

According to Howard Rosen, chairman of the Rail Working Group, a non-profit organization representing the railway industry, “I think east-west trade on the rail silk routes is growing faster than a lot of people expected. It’s a cascade—as you begin to get the system working, more people know about it and more business opportunities arise. The implications are even greater for west-east trade.”

In theory, any European city can be connected with China, though trains will still need to travel via hubs like Vienna, where work is being done to lay 1,520-mm gauge track (an old Soviet standard, which has traditionally stopped at the borders of Central Asian states). This would make it possible for the trains coming from the northern corridors, which follow the trans-Siberian route, to go all the way to Austria. Right now, they have to stop at Brest, on the Poland-Belarus border, and switch back to standard 1,435-mm gauge. Variable gauge wagons also could become more common and resolve incompatibility issues.

The regional initiatives are also becoming more connected. In addition to an expansion of the northern routes, such as a project linking Mongolia into a spur that joins the trans-Siberian corridor, a number of southern routes are planned that will connect CAREC countries. These will create corridors, and expand on nascent ones, that link China to Türkiye through Kazakhstan, Uzbekistan, Turkmenistan, Azerbaijan and Georgia, as well as routes that travel through Afghanistan to connect to ports in Iran and onto Europe by rail. Eventually, rail networks in Central Asia may even link with those in SASEC countries.

It is unlikely that rail freight will soon compete with container shipping on price or on volume. It is still around three to four times the cost of ocean freight, it still represents only 1.2 percent of cargo flows between Europe and Asia by volume and just over two percent by value. But for higher-value electronics, car parts or perishable food items, the faster times and improved reliability might justify a modal shift. “Rail offers a huge amount of flexibility,” says Mr. Rosen. “Unlike with ships, you can choreograph where cargo ends up. One part of a freight train from China may stop at a distribution point, such as Duisburg, while another part of it carries on to another city, say, Antwerp. Differentiated transport is far better suited as economies become more sophisticated.”

CAREC as engine for growth

This has implications for CAREC. Over the next decade, the economic logic of overland routes will probably warrant an expansion of infrastructure, both hard and soft. Services will become more regular and the increase in traffic should help bring prices down further. The countries along the southern corridors should be more motivated to invest in transport infrastructure, as they will be able to see the benefits it brings. National governments will need to become more aggressive about attracting investment and developing supporting industries, particularly around special economic zones and logistics hubs. They will need to improve the regulatory environment so that it facilitates cross-border trade and travel.

The long-term investment requirements to 2030 are estimated to be USD38 billion on the six designated rail corridors, and more for maintenance and upgrades. This comprises the 25,200 km that currently exist and another 7,200 that need to be built.

Failure to take action will mean missing out. “There is now a willingness throughout the region to explore greater connectivity,” says Mr. Moseley. “We should not underestimate the challenges: geographic, geopolitical, political and financing. But governments have realized that fostering additional trade can yield win-win benefits. And what we are seeing is a much more even-handed, multimodal approach.”

With the advent of new transport routes comes the opening of new markets that were previously inaccessible as land-locked regions, and land-locked countries within regions, become easier and faster to reach, potentially changing the nature of trade in Asia for decades to come.